This article considers the intricacies of AML transaction monitoring, looking at its significance, how it works, its benefits, and best practices when it comes to fine-tuning a solution to help safeguard the integrity of the global financial system.

What is AML transaction monitoring software?

AML transaction monitoring software refers to solutions that offer ongoing surveillance and analysis of transactions, which FIs use to detect and prevent financial crime. By leveraging advanced technological capabilities and comprehensive risk assessments, AML transaction monitoring aims to ensure compliance with regulatory obligations and mitigate the risk of firms processing transactions associated with bad actors.

How does a transaction monitoring solution work?

Multiple steps occur in transaction monitoring. Depending on the solution, the process looks like this:

Data collection: Transaction monitoring often begins with the collection of transactional data from various sources within the FI in question, including banking transactions, wire transfers, ATM withdrawals, and online payments.

Data aggregation: The collected data is then aggregated into a central database, where it can be accessed and analyzed efficiently. Depending on the sophistication of the software, this analysis can be done in real time using machine learning (ML). These ML algorithms can detect patterns of behavior as well as anomalous activity, helping compliance teams recognize potentially illicit activity in a fraction of the time.

Rule-based screening: AML transaction monitoring software often uses predefined rules and algorithms to screen transactions in real time or via batch processing. These rules are usually based on regulatory requirements and internal policies for the firm. For example, transactions above a particular threshold or those involving high-risk countries or entities may trigger alerts. However, a robust transaction monitoring program would also feature custom rule sets tailored to the firm’s risk appetite and business activity.

Anomaly detection: During the analysis stage, transactional behavior is compared against historical data and established profiles to detect deviations or anomalies.

Alert generation: When a transaction triggers a rule or is flagged as potentially suspicious, an alert is generated for further inspection by a compliance professional. Alerts typically include details of the transaction, the rule triggered, and any other contextual information. Depending on the software, these alerts can be prioritized depending on the potential seriousness of the incident. This helps analysts effectively prioritize their time and maintain higher levels of efficiency.

Investigation and resolution: Compliance officers then review the alerts to determine their legitimacy and assess the level of risk associated with the flagged transactions. This may involve gathering more information from internal and external sources, conducting customer due diligence (CDD), and deploying enhanced transaction monitoring measures.

Reporting: Once the investigation is complete, a decision has to be made on whether to submit a suspicious activity report (SAR) to the firm’s appropriate regulatory authority. Good AML transaction monitoring software will often facilitate the generation and submission of SARs, helping firms meet their regulatory obligations.

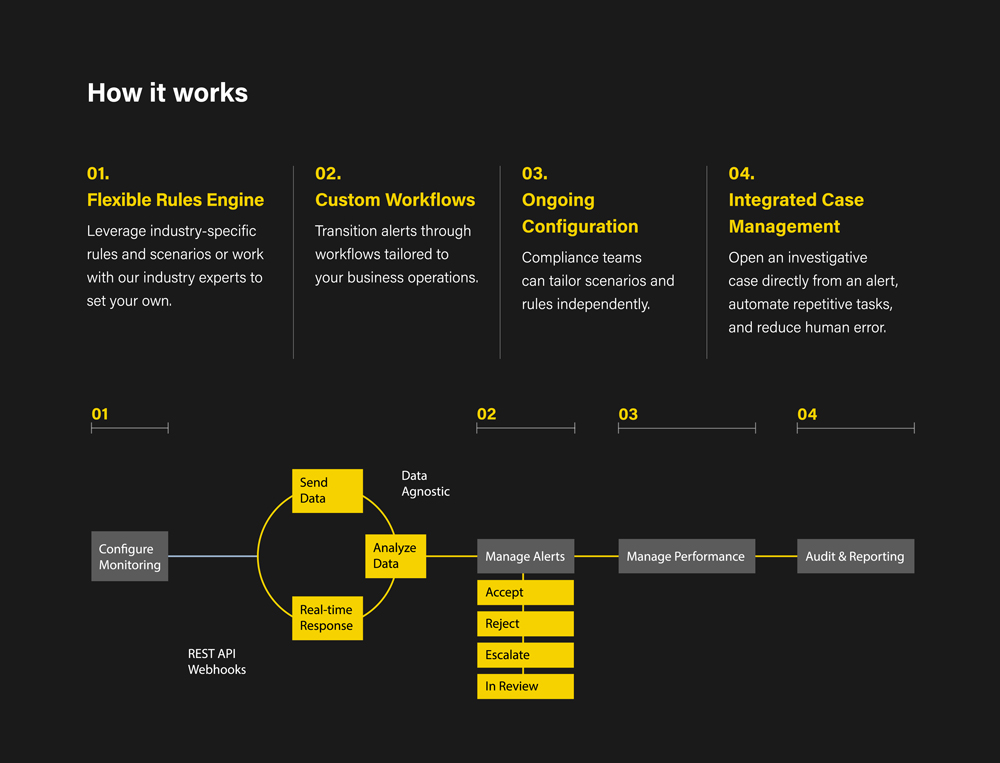

For additional context, here is a condensed visualization of how ComplyAdvantage’s Transaction Monitoring solution works.

Why is AML transaction monitoring software important?

Regulators and international organizations, such as the Financial Action Task Force (FATF), consistently emphasize the importance of utilizing robust AML transaction monitoring software. The FATF’s 40 Recommendations include references to such software, encouraging firms to “scrutinize transactions undertaken throughout the course” of a business relationship. To do this effectively, the FATF recognizes the potential of harnessing artificial intelligence (AI) and machine learning (ML)-based solutions to strengthen transaction monitoring and other compliance processes. In fact, according to the FATF,

A responsible use of new technologies, including digital identity and cutting-edge transaction monitoring and analysis solutions (including collaborative analytics) can assist effective, risk-based implementation of the FATF Standards by the public and private sectors, as well as promote financial inclusion.

But aside from effectively meeting the FATF’s standards, why else is AML transaction monitoring software important?

Enhances regulatory compliance: Regulators worldwide require FIs to implement effective AML controls to prevent money laundering, terrorist financing, and other financial crimes. For example, under the Bank Secrecy Act, firms must file reports to the Financial Crimes Enforcement Network (FinCEN) of any cash transactions exceeding $10,000. To ensure compliance with this requirement, firms can create rules within their transaction monitoring software to alert compliance teams when a transaction of this amount or higher is being attempted.

Mitigates reputational risk: When illicit financial activity is missed or left unchecked, it can greatly affect a firm’s reputation in the industry – not just through the eyes of regulators but stakeholders and customers too. By proactively addressing potentially suspicious activity with a robust transaction monitoring solution, firms can demonstrate their commitment to regulations, ethical standards, and customer protection.

Supports enhanced due diligence (EDD): By integrating transaction monitoring with due diligence processes, firms can ensure a more comprehensive understanding of their customers’ financial behaviors, allowing for timely and appropriate risk assessments. This helps meet regulatory requirements and strengthens the firm’s ability to mitigate risks, ensuring a robust defense against financial crimes and enhancing overall operational integrity.

Detects emerging financial crime typologies: As criminals continuously adapt their strategies to bypass traditional security measures, transaction monitoring systems can analyze large volumes of transaction data in real-time to spot anomalous patterns and behaviors indicative of emerging threats. This continuous vigilance enables firms to stay ahead of sophisticated fraud schemes and money laundering techniques, ensuring timely adaptation to new risks.

The best transaction monitoring software and companies in 2024

Compare the key strengths of the 6 top transaction monitoring software vendors.

What are the key features of an effective transaction monitoring software?

An effective AML transaction monitoring software should incorporate several key features to meet the requirements of its users:

Advanced AI and ML: These algorithms enable the software to learn from data patterns continuously, adapt to evolving threats, and improve accuracy as time passes.

Flexibility: The software should offer flexibility in terms of customization, allowing users to tailor detection rules, thresholds, and risk parameters to their specific business requirements and compliance standards.

One platform: A single, integrated platform for transaction monitoring streamlines operations by consolidating data sources, alert management, and reporting capabilities into one centralized location.

Real-time monitoring: To analyze transactions as they occur, allowing for instant detection and response to suspicious activity.

Customizable alerts: These enable users to define alert thresholds, escalation processes, and notification preferences based on their risk appetite and operational needs.

Easy integration: With existing systems and data sources, such as core platforms, customer relationship management (CRM) databases, and third-party data providers.

User-friendly interface: An intuitive and user-friendly interface simplifies navigation, facilitates ease of use, and reduces training time.

Customer support: When comparing vendors, FIs should ensure the preferred vendor offers implementation assistance, continuous support, and aftercare, viewing it as an ongoing partnership rather than a transaction.

How does transaction monitoring software interact with human AML expertise?

To create a robust defense against financial crime, transaction monitoring software should interact with human AML expertise. But what does this look like? Typically, the software should scan transactions for suspicious patterns and anomalies and generate alerts for further investigation by AML experts. These compliance professionals then use their judgment to determine the need for action, enhancing decision-making with the software’s data.

Experts can also fine-tune the software’s algorithms to help reduce false positives and improve accuracy, reflecting current or emerging threats and regulatory requirements. The software presents data in a user-friendly format, aiding comprehensive investigations and efficient case building. A dynamic feedback loop also allows AML professionals to provide insights that refine the software, leading to continuous improvement.

Additionally, transaction monitoring software serves as a training tool, helping experts stay updated on emerging typologies and regulatory changes. This connection between automated analysis and human expertise ensures a comprehensive and adaptive AML strategy, effectively combating financial crimes.

Improve your organization’s operational efficiency

Fortify your organization and fuel your growth with dynamic solutions tailored to your needs. Book your free demo today and find out why 1000s already use ComplyAdvantage.

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

EN

EN FR

FR

Featured

Featured